All Categories

Featured

Table of Contents

- – How can an Variable Annuities protect my retir...

- – Is there a budget-friendly Lifetime Payout Ann...

- – How much does an Annuity Investment pay annua...

- – Where can I buy affordable Guaranteed Income ...

- – How can an Fixed Vs Variable Annuities help ...

- – How can an Secure Annuities help me with est...

Keep in mind, however, that this doesn't say anything about readjusting for inflation. On the plus side, even if you presume your choice would certainly be to purchase the stock exchange for those seven years, which you would certainly get a 10 percent yearly return (which is much from certain, especially in the coming years), this $8208 a year would certainly be greater than 4 percent of the resulting nominal supply value.

Instance of a single-premium deferred annuity (with a 25-year deferral), with 4 payment alternatives. The monthly payment here is highest possible for the "joint-life-only" option, at $1258 (164 percent higher than with the immediate annuity).

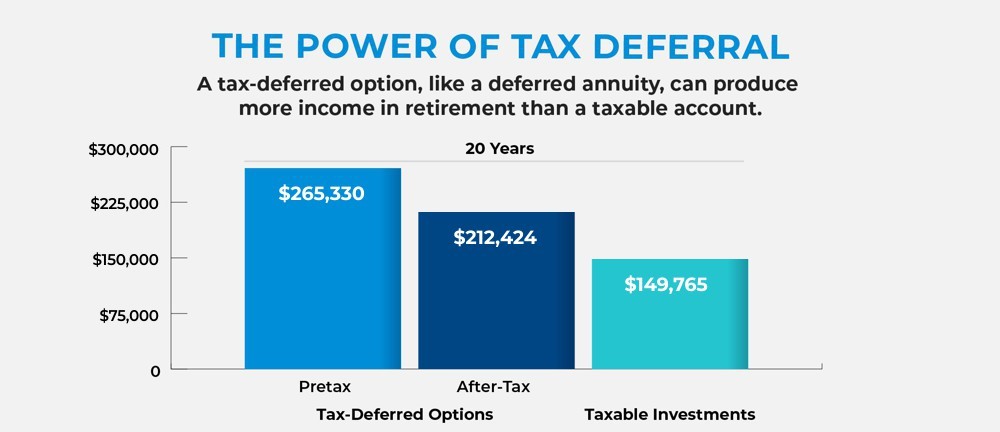

The means you acquire the annuity will figure out the response to that inquiry. If you buy an annuity with pre-tax dollars, your costs minimizes your taxed revenue for that year. Nevertheless, eventual settlements (month-to-month and/or round figure) are exhausted as normal earnings in the year they're paid. The benefit below is that the annuity may let you postpone taxes past the IRS payment restrictions on IRAs and 401(k) strategies.

According to , buying an annuity inside a Roth strategy causes tax-free payments. Getting an annuity with after-tax dollars beyond a Roth leads to paying no tax on the part of each settlement credited to the original costs(s), yet the remaining section is taxable. If you're setting up an annuity that begins paying before you're 59 years old, you may need to pay 10 percent very early withdrawal charges to the internal revenue service.

How can an Variable Annuities protect my retirement?

The expert's initial step was to establish a detailed monetary strategy for you, and then describe (a) exactly how the recommended annuity suits your total strategy, (b) what alternatives s/he taken into consideration, and (c) how such alternatives would or would not have actually led to lower or greater payment for the advisor, and (d) why the annuity is the exceptional option for you. - Guaranteed return annuities

Of training course, an advisor might try pressing annuities also if they're not the very best fit for your circumstance and goals. The reason could be as benign as it is the only product they sell, so they fall target to the proverbial, "If all you have in your tool kit is a hammer, pretty soon every little thing begins resembling a nail." While the advisor in this scenario might not be dishonest, it enhances the threat that an annuity is a poor option for you.

Is there a budget-friendly Lifetime Payout Annuities option?

:max_bytes(150000):strip_icc()/Term-a-annuity-d4d5906faea940828244ef128f416cc5.jpg)

Since annuities commonly pay the agent marketing them much greater compensations than what s/he would obtain for spending your cash in mutual funds - Guaranteed income annuities, not to mention the zero commissions s/he 'd obtain if you buy no-load common funds, there is a big reward for representatives to push annuities, and the much more difficult the much better ()

A deceitful consultant recommends rolling that quantity right into brand-new "far better" funds that simply occur to bring a 4 percent sales lots. Concur to this, and the consultant pockets $20,000 of your $500,000, and the funds aren't likely to perform better (unless you selected much more improperly to start with). In the exact same instance, the advisor could steer you to acquire a complicated annuity with that $500,000, one that pays him or her an 8 percent commission.

The consultant attempts to rush your choice, claiming the offer will quickly vanish. It may indeed, but there will likely be equivalent offers later on. The advisor hasn't determined just how annuity payments will certainly be taxed. The advisor hasn't revealed his/her compensation and/or the charges you'll be billed and/or hasn't shown you the influence of those on your eventual payments, and/or the payment and/or charges are unacceptably high.

Your family members history and present health indicate a lower-than-average life span (Guaranteed return annuities). Present rate of interest prices, and thus predicted settlements, are traditionally reduced. Even if an annuity is appropriate for you, do your due diligence in comparing annuities offered by brokers vs. no-load ones offered by the releasing business. The latter may require you to do more of your very own research study, or make use of a fee-based economic consultant that may receive compensation for sending you to the annuity company, but might not be paid a higher commission than for other investment options.

How much does an Annuity Investment pay annually?

:max_bytes(150000):strip_icc()/Immediate-variable-annuity.asp-final-c62d88ef3f7a4b688c0303ef04e1fbce.png)

The stream of month-to-month repayments from Social Safety resembles those of a delayed annuity. A 2017 relative evaluation made an extensive comparison. The following are a few of the most prominent factors. Because annuities are volunteer, individuals purchasing them usually self-select as having a longer-than-average life span.

Social Protection benefits are fully indexed to the CPI, while annuities either have no inflation security or at many provide a set portion yearly boost that may or may not compensate for inflation completely. This type of biker, as with anything else that boosts the insurance firm's threat, needs you to pay even more for the annuity, or approve reduced settlements.

Where can I buy affordable Guaranteed Income Annuities?

Please note: This short article is intended for informational objectives just, and must not be considered financial recommendations. You need to consult a financial expert prior to making any type of major monetary choices. My occupation has actually had many uncertain twists and turns. A MSc in academic physics, PhD in experimental high-energy physics, postdoc in bit detector R&D, research setting in speculative cosmic-ray physics (including a number of sees to Antarctica), a short job at a tiny engineering solutions firm supporting NASA, complied with by starting my very own small consulting technique supporting NASA jobs and programs.

Because annuities are planned for retirement, taxes and charges might apply. Principal Security of Fixed Annuities.

Immediate annuities. Deferred annuities: For those that desire to expand their money over time, however are eager to delay access to the money until retired life years.

How can an Fixed Vs Variable Annuities help me with estate planning?

Variable annuities: Gives better potential for development by spending your cash in financial investment alternatives you select and the capability to rebalance your profile based on your choices and in such a way that aligns with altering financial objectives. With taken care of annuities, the company invests the funds and supplies a rate of interest to the client.

When a fatality case takes place with an annuity, it is vital to have a named beneficiary in the contract. Different options exist for annuity fatality benefits, depending upon the contract and insurer. Selecting a reimbursement or "duration specific" choice in your annuity provides a survivor benefit if you pass away early.

How can an Secure Annuities help me with estate planning?

Naming a recipient other than the estate can help this procedure go a lot more smoothly, and can assist ensure that the earnings go to whoever the specific wanted the cash to go to instead than going with probate. When existing, a fatality advantage is automatically consisted of with your contract.

{kind=link}

Table of Contents

- – How can an Variable Annuities protect my retir...

- – Is there a budget-friendly Lifetime Payout Ann...

- – How much does an Annuity Investment pay annua...

- – Where can I buy affordable Guaranteed Income ...

- – How can an Fixed Vs Variable Annuities help ...

- – How can an Secure Annuities help me with est...

Latest Posts

Decoding Variable Annuity Vs Fixed Annuity Everything You Need to Know About Fixed Interest Annuity Vs Variable Investment Annuity Defining Annuities Variable Vs Fixed Advantages and Disadvantages of

Breaking Down Annuities Variable Vs Fixed Everything You Need to Know About Fixed Index Annuity Vs Variable Annuity Breaking Down the Basics of Fixed Indexed Annuity Vs Market-variable Annuity Feature

Highlighting Fixed Vs Variable Annuities A Closer Look at How Retirement Planning Works What Is Fixed Indexed Annuity Vs Market-variable Annuity? Features of What Is Variable Annuity Vs Fixed Annuity

More

Latest Posts